Lane Departure Warning System Market is expected to reach US$ 17096.38 Mn. by 2026, at a CAGR of 23.1% during the forecast period.

Market Size

- 2024 Estimated Value: USD 4.6 Billion

- 2033 Forecast Value: USD 17.8 Billion

- Compound Annual Growth Rate (2025–2033): Estimated between 6% to 14%, most commonly around 10–12%

Overview

Lane Departure Warning Systems (LDWS) are critical elements of Advanced Driver Assistance Systems (ADAS). Utilizing cameras and sensors, they detect unintended lane drifting and alert drivers through audio, visual, or haptic feedback. Evolving into Lane Keeping Systems (LKS) and Lane Centering Assist (LCA), some systems now actively steer vehicles to return to the correct lane.

To Know More About This Report Request A Free Sample Copy https://www.maximizemarketresearch.com/request-sample/107504/

Market Estimation & Definition

This global market includes LDWS, LKS, Lane Centering Assist (LCA), and Automated Lane Keeping Systems (ALKS), supplied by OEMs or the aftermarket. These systems integrate video cameras, infrared sensors, radar, and AI-based algorithms to improve vehicle safety across both passenger and commercial vehicles.

Market Growth Drivers & Opportunity

- Regulatory Pressures: Global regulations are increasingly mandating LDWS/LKS in new vehicles to improve road safety.

- Accident Reduction Impact: Studies indicate LDWS can prevent a notable percentage of lane-departure collisions, particularly in trucks and passenger cars.

- ADAS & Autonomous Tech Integration: LDWS serves as a foundational technology for higher-level autonomy, creating crossover opportunities with ADAS providers.

- Sensor Fusion Enhancements: Advanced integration of vision, radar, and AI is improving system accuracy and performance.

- Consumer Safety Awareness: As safety becomes a higher purchasing factor in mid-range vehicle segments, LDWS adoption is becoming widespread.

Segmentation Analysis

By System Type:

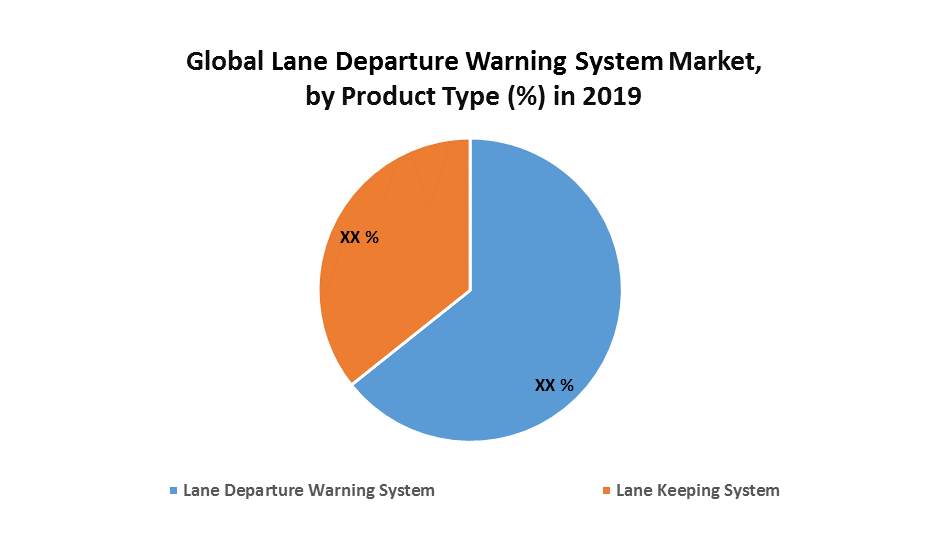

- Lane Departure Warning (LDW) – ~40% share

- Lane Keeping System (LKS) – ~35%

- Lane Centering Assist (LCA) – ~20%

By Sensor Type:

- Video Camera – primary sensor

- Infrared – significant usage

- Radar/Laser fusion – advanced systems

By Vehicle Type:

- Passenger Vehicles – dominant segment

- Commercial Vehicles (LCVs, HCVs) – growing adoption

By Distribution Channel:

- OEM – around 80% of market share

- Aftermarket – high growth potential

By Region:

- North America – largest by revenue (~35%)

- Asia-Pacific – fastest-growing, 15%+ CAGR

- Europe – robust growth with regulatory support (~25%)

- Latin America & MEA – emerging markets (~10%)

Major Manufacturers

- Autoliv

- Continental

- Robert Bosch

- Mobileye (Intel)

- Denso

- Delphi/BorgWarner

- Hitachi

- ZF Friedrichshafen

- Magna International

- Iteris

- Key regional automakers and Tier-1 ADAS suppliers

Regional Analysis

North America:

The leading region, bolstered by supportive safety regulations, widespread truck usage with ADAS, and strong aftermarket presence.

Europe:

High deployment due to UNECE mandates and widespread LKS adoption. Infrared and camera-based systems excel in European regulatory environments.

Asia-Pacific:

Rapid vehicle production and safety initiatives in China, India, Japan, and South Korea fuel high growth and MID-market LDWS integration.

Latin America & MEA:

Gradual but accelerating adoption driven by rising vehicle safety awareness and improving road infrastructure.

COVID‑19 Impact Analysis

Initial production slowdowns and vehicle sales dips occurred during the pandemic. However, LDWS installations rebounded strongly as automakers refocused on ADAS safety and resumed production of vehicles equipped with such systems.

Commutator Analysis

LDWS relies entirely on digital sensors and software mechanisms rather than mechanical commutation:

- Vision Modules: High-definition cameras identify lane markings

- Sensor Fusion: Infrared, radar, and image analytics combine for robust detection

- AI Algorithms: Real-time steering input calculation

- Driver Alerts: Haptic, visual, or auditory warnings via ECUs

- Active Steering Integration: LKS/LCA modules actively control lane positioning

Key Questions Answered

- What is the market size by 2033?

USD 17.8 Billion - What CAGR is projected?

Between 6% and 14%, typically around 10–12% - Which system types dominate?

LDW (~40%) and LKS (~35%), with LCA gaining momentum - Which sensor type is most common?

Video cameras, followed by infrared and radar/lidar fusion - Which regions lead and grow fastest?

North America leads; Asia-Pacific grows fastest - How did COVID-19 affect the market?

Short-term disruptions followed by renewed focus on vehicle safety and ADAS features - What trends are shaping the future?

Sensor fusion, AI-driven autonomy, OEM-led adoption, and cost-effective mid‑market solutions

Conclusion

The Lane Departure Warning System market is set for robust expansion—forecast to nearly quadruple by 2033. With growing regulatory mandates, ADAS integration, and sensor-fusion capabilities, this market presents substantial opportunities for Tier-1 suppliers, OEMs, and aftermarket innovators. The competitive edge will go to those offering affordable, AI-enhanced, and reliable LDWS solutions for a global vehicular landscape.

About Maximize Market Research:

Maximize Market Research is a global market research and consulting company specializing in data-driven insights and strategic analysis. With a team of experienced analysts and industry experts, the company provides comprehensive reports across various sectors, aiding businesses in making informed decisions and achieving sustainable growth.

Contact Us

Maximize Market Research Pvt. Ltd.

2nd Floor, Navale IT Park, Phase 3

Pune-Bangalore Highway, Narhe

Pune, Maharashtra 411041, India

📞 +91 96073 65656

✉️ sales@maximizemarketresearch.com